OpenSCHUFA – shedding light on Germany’s opaque credit scoring

Why we started OpenSCHUFA, why you should care about credit scoring & how you can help.

Why we started OpenSCHUFA, why you should care about credit scoring & how you can help.

Germany's leading credit bureau, SCHUFA, has immense power over people's lives. A low SCHUFA score means landlords will refuse to rent you an apartment, banks will reject your credit card application and network providers will say 'no' to a new Internet contract. But what if your SCHUFA score is low because there are mistakes in your credit history? Or if the score is calculated by a mathematical model that is biased?

The big problem is, we simply don't know how accurate SCHUFA's data is and how it computes its scores. No one does, not even the German government. OpenSCHUFA wants to change this by analyzing thousands of credit records.

To do this, we need your help.

How can I help?

- Not living in Germany?

Please donate somey money - 5 EUR (6 USD) or more - to enable us to develop a data-donation software (Open Source and reusable in your country). Get in touch, if you interested in a similar campaign on the credit bureau in your country: info@openschufa.de - Order for your SCHUFA credit record now, donate it later

We need as many people living in Germany as possible to order their SCHUFA credit record and donate the record to OpenSCHUFA . The more records we can evaluate, the more accurate our findings will be, and the more comprehensible SCHUFA’s scoring process will become for everyone. You can immediately orderask for your free SCHUFA credit record by going to selbstauskunft.net. It will take some weeks to arrive by postal mail. Once the data donation platform is ready in May 2018 (financed by your Euro donations) you’ll be able to upload your credit record together with some demographic information we need to make sense of the data. (Read more on how to do this below.) - Donate 5 euro (or more) to OpenSCHUFA on the crowdfunding platform, Startnext

We want to raise 50,000 Euro (61,700 USD) in two steps (1st: 30.000 Euro) to help pay for the project through a campaign on Startnext, a German crowdfunding platform (Link - text in English). The donations will be used for various aspects of the project, such as developing the software to collate and read the credit records, pay data analysts and publish the results. We'll release the software under an open source license so that others around the world can use it in similar transparency projects - Share your SCHUFA stories

We want to hear about your experiences with SCHUFA – if you have found incorrect information in the past, or had problems getting credit because of your SCHUFA record. We would also love tenants associations, housing services and consumer protection agencies to share their stories. Get in touch by emailing us at info@openschufa.de.

What exactly is SCHUFA?

SCHUFA is Germany's leading credit bureau. It's a private company similar to Equifax, Experian or TransUnion, some of the major credit reporting agencies operating in the US, UK, Canada or Australia.

SCHUFA collects data of your financial history – your unpaid bills, credit cards, loans, fines and court judgments – and uses this information to calculate your SCHUFA score. Companies pay to check your SCHUFA score when you apply for a credit card, a new phone or Internet contract. A rental agent even checks with SCHUFA when you apply to rent an apartment. A low score means you have a high risk of defaulting on payments, so it makes it more difficult, or even impossible, to get credit. A low score can also affect how much interest you pay on a loan.

The name SCHUFA comes from an abbreviation of its German title, "Schutzorganisation für Allgemeine Kreditsicherung". This roughly translates as "Protection Agency for General Credit Security".

Why should I care about SCHUFA and its credit scores?

SCHUFA holds data on round about 70 million people in Germany. That's nearly everyone in the country aged 18 or older. According to SCHUFA, nearly one in ten of these people living in Germany (some 7 million people) have negative entries in their record. That's a lot!

SCHUFA gets its data from some 9,000 partners, such as banks and telecommunication companies. Incredibly, SCHUFA doesn't believe it has a responsibility to check the accuracy of data it receives from its partners.

In addition, the algorithm used by SCHUFA to calculate credit scores is protected as a trade secret so no one knows how the algorithm works and whether there are errors or injustices built into the model or the software.

So basically, if you are an adult living in Germany, it's a good chance your financial life is affected by a credit score produced by a multimillion euro private company using an automatic process that they do not have to explain and an algorithm based on data that nobody checks for inaccuracies.

How can I donate my SCHUFA record?

STEP ONE: Order your SCHUFA record

- Everyone in Germany is entitled to obtain a free copy of their credit record once a year (you can apply more often, but you have to pay a fee after the first application).

- The easiest way to apply is to use the site selbstauskunft.net (in German).

- After a few weeks, you will receive a copy of your SCHUFA credit record in the post.

STEP TWO: Upload your SCHUFA record to OpenSCHUFA

- Go to our site OpenSCHUFA.de, which will offer the upload functionality in May 2018.

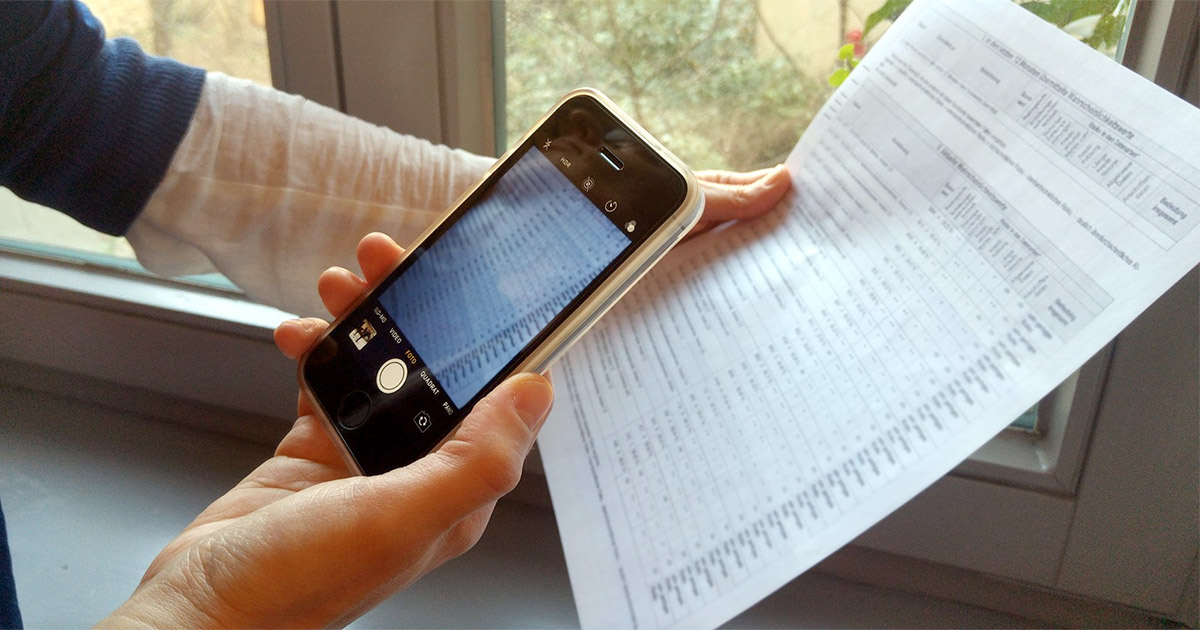

- Scan or take a photo of your credit record (the main table, no personal data)

- Upload it to the site

- We will ask a few questions about you, such as your age, gender, country of birth, income, postcode, number of children, number of mobile phone contracts, how often you have moved in the past two years, how many lines of credit you open and how often you have missed credit payments. Providing this data will be completely voluntary but the more you provide, the more it will help us analyze SCHUFA's algorithm for discrimination.How easy is that!

What will OpenSCHUFA do with my data?

OpenSCHUFA has gathered a group of data scientists, including data journalists from Bayerischer Runkfunk, a state broadcaster, and Spiegel Online, the German news site, who will analyze the credit data together with us.

We start publishing the first findings around July, with the final evaluation in November 2018. We will also try to make as much of the data as possible available as open data for other researchers to use – but only data that cannot be traced back to an individual.

How will you protect my data and make it anonymous?

We are only interested in the main table of your SCHUFA record. We are not interested in your name, your birth date or your address. We will ask for additional demographic information to be able to analyse the data of the SCHUFA record more exact, to ascertain how different profiles are treated differently by the SCHUFA. Your identity is not relevant for us.

The data you donate to OpenSCHUFA will only used to analyze the SCHUFA scoring process. It will neither be forwarded to third parties nor sold. The data will be transferred with an end-to-end encryption and stored on our server.

Who initiated OpenSCHUFA?

- Open Knowledge Foundation Germany okfn.de – a non-profit organization that advocates for open knowledge, open data, transparency and civil participation

• AlgorithmWatch – a German-based non-profit that evaluates and sheds light on algorithmic and automatization processes with social relevance

If you have any question, please get in touch by info@openschufa.de